Provision of Professional Services to Medical Marijuana Dispensaries by Arizona CPA’s (March 2016)

Issue:

Chapter 28 of Title 36, Public Health and Safety of the Arizona Revised Statutes (“ARS”), entitled Arizona Medical Marijuana

Act, legalizes in the State of Arizona the sale and use of medical marijuana which such sale being authorized through

registered nonprofit medical marijuana dispensaries. Title 9, Health Services, Chapter 17, Department of Health Services

Medical Marijuana Program of the Arizona Administrative Code, authorized by ARS 36-2803 provides regulations that medical

marijuana dispensaries must abide by. Rule R9-17-308 (B)(4) states that to renew the license of a medical marijuana dispensary,

such entity must provide, “A report of an audit by an independent certified public accountant of the annual financial statements

required in subsection (B)(3).”

However, the sale of marijuana, whether for medicinal purposes or recreational purposes, is

still illegal under United States Federal Laws. Consequently, Arizona CPA’s have questioned whether the provision of the

aforementioned audit services as well as other accounting services by Arizona CPA registrants would be considered an act

discreditable should they provide such services to such entities. For purposes of this white paper, the term accounting services

should be considered as defined within ARS 32-701 to mean:

“services that are commonly and historically performed by accountants,

including recording or summarizing financial transactions, bookkeeping, analyzing or verifying financial information, auditing,

reviewing or compiling financial statements, reporting financial results, financial planning, providing attestation or tax or

consulting services.”

Materials Considered by the Arizona Board of Accountancy:

During its considerations of this matter, the Arizona Board of Accountancy has considered the following materials:

1. An Issue Brief on State Marijuana Laws and the CPA Profession, Issued May 16, 2013 and last updated January 5, 2015 which was

issued by the American Institute of Certified Public Accountants and the Colorado and Washington State Societies of Certified

Public Accountants;

2. An Issue Brief on State Marijuana Laws and the CPA Profession, Issued July 24, 2015 and last updated January 8, 2016 which

was issued by the American Institute of Certified Public Accountants and the Colorado and Washington State Societies of Certified

Public Accountants;

3. FIN-2014-G001 Guidance issued February 14, 2014 by Department of the Treasury Financial Crimes Enforcement Network entitled,

BSA Expectations Regarding Marijuana-Related Businesses;

4. State Bar of Arizona Ethics Opinions 11-01: Scope of Representation, 2/2011 regarding legal ethics of a lawyer counselling or

assisting a client;

5. Business Appraisal Within the Cannabis Industry: The ultimate appraisal challenge issued by Ronald L. Seigneur of Seigneur

Gustafson LLP, copyright 2015;

6. Obstacles to Legalizing Marijuana: Resolving the Federal-State Conflict Authored by Wei-Chih Chiang and produced in the

Checkpoint subscription service in May 2015;

7. AICPA: Talking to State Boards About Marijuana Policies: Key Policy Suggestions for State CPA Societies; and

8. AICPA: Providing Services to Businesses in the Marijuana Industry: A Sample of Current Board Positions.

Powers of the Arizona Board of Accountancy

Under ARS 32-741, the Board may revoke or suspend a registrant’s certificate, take disciplinary action or issue a letter of

concern for numerous causes that are enumerated therein and include, but are not limited to conviction of a felony, conviction

of a crime with a reasonable relationship to the practice of accounting, dishonesty, suspension or revocation for cause of the

right to practice before a governmental body or agency and other acts. Further, regulation R4-1-455.03 entitled Discreditable

Acts states that a registrant shall not commit an act that reflects adversely on the registrant’s fitness to engage in the

practice of public accounting which includes violating ARS Title 32, Chapter 6, Article 3 as well as various enumerated rules.

Conclusion:

The authorized sale of medical marijuana is legal in the State of Arizona and the State of Arizona has mandated that such sale

be performed by licensed and regulated medical marijuana dispensaries. Further, the State of Arizona has mandated that to renew

their license such medical marijuana dispensaries must retain a certified public accountant to perform an audit of the financial

statements of such entity. The Arizona Board of Accountancy recognizes that while the state of Arizona has a law that legalizes the

sale of medical marijuana, the Federal Government does not have such a law. As there is a dichotomy between Federal and Arizona law,

the Arizona Board of Accountancy can make no determination of how such a conflict might ultimately affect a medical marijuana

dispensary or any of its service providers. Hence, the Arizona Board of Accountancy has concluded that during the contemplation of

acceptance of any accounting services engagement for a medical marijuana dispensary, an Arizona registrant should diligently evaluate

and address the potential risks and uncertainties associated with providing such services. Registrants should carefully consider the

criteria provided in auditing standards and other professional materials, as well as professional guidance specifically related to

providing services to the medical marijuana industry. Further, the Arizona Board of Accountancy has concluded that merely accepting an

engagement to provide accounting services to a medical marijuana dispensary does not, on its face, constitute an act discreditable to

the profession and it will not pursue independent disciplinary action against an Arizona CPA registrant based solely on such acceptance.

The Arizona Board of Accountancy recommends that Arizona registrants considering providing services to the medical marijuana industry

read the materials referenced herein, professional standards applicable to the professional services to be provided and guidance offered

by State and Federal regulatory bodies, including, but not limited to the Internal Revenue Service, the U.S. Department of Justice and

the U.S. Securities Exchange Commission and any other authoritative materials available that frame the issues contemplated herein.

Issuance Date:

March 28, 2016

Board's Portal and Renewals Online (July 2012)

The Arizona State Board of Accountancy (Board) is pleased to announce the

release of its portal which represents the exciting completion of the first of

many milestones to modernize the Board’s operations and improve services to its

customers. The portal, currently in its infancy, provides services for online

renewals, and sole practitioner firm registration if applicable as part of the

online renewal, as well as CPE tracking. The system currently can be used by

registrants with full two year term renewals. The system cannot be used by

registrants, who have recently been certified and have a prorated renewal period

and prorated CPE requirements, however, the system is being enhanced to

accommodate these registrants in the near future. The portal is being

strategically designed as an online account that will be unique to each and

every customer of the Board whether they are an applicant to sit for the uniform

CPA exam, a certification candidate, or a registrant already regulated by the

Board.

The Arizona State Board of Accountancy (Board) is pleased to announce the

release of its portal which represents the exciting completion of the first of

many milestones to modernize the Board’s operations and improve services to its

customers. The portal, currently in its infancy, provides services for online

renewals, and sole practitioner firm registration if applicable as part of the

online renewal, as well as CPE tracking. The system currently can be used by

registrants with full two year term renewals. The system cannot be used by

registrants, who have recently been certified and have a prorated renewal period

and prorated CPE requirements, however, the system is being enhanced to

accommodate these registrants in the near future. The portal is being

strategically designed as an online account that will be unique to each and

every customer of the Board whether they are an applicant to sit for the uniform

CPA exam, a certification candidate, or a registrant already regulated by the

Board.

As the Board continues its modernization efforts, the services in the portal

will continue to grow. For example, in the future the portal will include other

online applications or a quick and convenient place to update a name or address

with a few simple steps. These changes help the Board work smarter and more

efficiently, improve regulation, and provide a more flexible and convenient

customer service experience.

During the summer, CPAs will receive a letter with an account number and

password which will require that the portal be used for renewals and CPE

tracking. Please be patient if you learn that another CPA has received this

information and you haven’t. The mailing will be a large endeavor for Board

staff and may be staggered over several weeks to complete.

The following delineates a few of the highlights of the new business processes

that are both advantageous to the Board and its customers and provide a win-win

solution.

Registration Renewal/Sole Practitioner Firm Registration

Convenience

- Provides customized forms that are dynamic based

on individual responses.

- Take a break and continue at a later time as entries

are saved as you go.

- MasterCard and Visa are accepted. Checks and cash are

still accepted by mail or in person after the renewal is

completed online and printed.

- E-file helps registrants avoid being late by ensuring instant

delivery and by saving time from mailing or hand delivery.

Transparency

All available renewal options (e.g., inactive, fee and continuing

professional education (CPE) waivers) are presented and fully described

to help CPAs make the most informed decisions about their license.

Customer Service

- Built-in help is always available for further clarification or guidance without having to call, email or wait until the Board’s office is open. Of course, Board staff is available to provide

personal assistance during business hours, if needed.

- The online renewal form integrates all the related forms that previously had to be downloaded separately, providing a one-stop experience.

- A confirmation receipt is emailed after the renewal is received and paid online.

Compliance and Efficiency

- Immediate validation of requirements ensures that renewals are complete and accurate before the renewal can be accepted.

- No lost or misplaced paperwork. The renewal is accessed through the Internet via a secured account number

Continuing Professional Education List

Since the web based model is replacing the paper based renewal and Excel CPE reporting forms,

all CPAs should access the portal and begin to track their CPE online even if their renewal

won’t be due for some time. The biggest transition issue with changing business processes

relates to CPE tracking, especially for those registrants whose renewals are due shortly

and may have already used the Excel CPE form to record their CPE. The recording of CPE

online is a one time transition issue but can be minimized for those CPAs that use the

CPE List portal application sooner rather than later. The sooner CPAs begin to use the

portal to track CPE, the more streamlined their next renewal will be as they will

minimize the need to reenter data. Additionally, two new fields including sponsoring

organization and location of program have been added to the required tracking elements

so the old form is obsolete by way of required content.

Since the web based model is replacing the paper based renewal and Excel CPE reporting forms,

all CPAs should access the portal and begin to track their CPE online even if their renewal

won’t be due for some time. The biggest transition issue with changing business processes

relates to CPE tracking, especially for those registrants whose renewals are due shortly

and may have already used the Excel CPE form to record their CPE. The recording of CPE

online is a one time transition issue but can be minimized for those CPAs that use the

CPE List portal application sooner rather than later. The sooner CPAs begin to use the

portal to track CPE, the more streamlined their next renewal will be as they will

minimize the need to reenter data. Additionally, two new fields including sponsoring

organization and location of program have been added to the required tracking elements

so the old form is obsolete by way of required content.

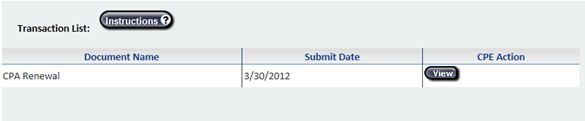

Transaction List

The transaction list is a feature where CPAs can find copies

of their most recent online transactions with the Arizona State

Board of Accountancy. The Board of Accountancy is undergoing a

multi-year modernization effort and over time other online transactions

will be added to the portal. However, the transaction list for the

time being will only include copies of your online renewal.

As such, if you lose your hard copy and need to print another

copy for your files then one can be found in your account under the transaction list button.

The Board has received positive reviews during the roll out of this new business

process. The online renewal has a survey to collect feedback to support the Board's

effort to better serve its customers through continuous improvement. The Board hopes

that CPAs enjoy this new process, and looks forward to hearing from them about their

experiences.

The transaction list is a feature where CPAs can find copies

of their most recent online transactions with the Arizona State

Board of Accountancy. The Board of Accountancy is undergoing a

multi-year modernization effort and over time other online transactions

will be added to the portal. However, the transaction list for the

time being will only include copies of your online renewal.

As such, if you lose your hard copy and need to print another

copy for your files then one can be found in your account under the transaction list button.

The Board has received positive reviews during the roll out of this new business

process. The online renewal has a survey to collect feedback to support the Board's

effort to better serve its customers through continuous improvement. The Board hopes

that CPAs enjoy this new process, and looks forward to hearing from them about their

experiences.